Workmens Comp

Table of Contents

Workers’ Compensation Essentials for Small Employers

A critical piece of that responsibility is workers’ compensation. For small employers, having the right workmens comp coverage is not just a box to check, it is a fundamental part of protecting your team and your business. According to the U.S. Department of Labor, workers’ compensation is a state-mandated, no-fault insurance program designed to provide medical benefits and wage replacement to employees who suffer a workplace injury or illness.

Most states require employers to carry workers compensation insurance, even for businesses with just a few employees. This workplace injury coverage is a two-way shield: it pays for an injured employee’s medical expenses, rehabilitation costs, and a portion of their lost wages, while simultaneously protecting the employer from direct lawsuits related to the incident. For a small business, this financial predictability is essential, as a single uninsured claim could be devastating.

Compliance is not optional, and the penalties for failing to maintain proper workers’ comp coverage can include significant fines, stop-work orders, or even personal liability for the business owner. This is where expert workers comp administration becomes invaluable. Understanding these essentials is the first step; the next is managing claims efficiently, and we become an extension of your team to handle this complex burden.

Understanding Workers’ Compensation Insurance Requirements

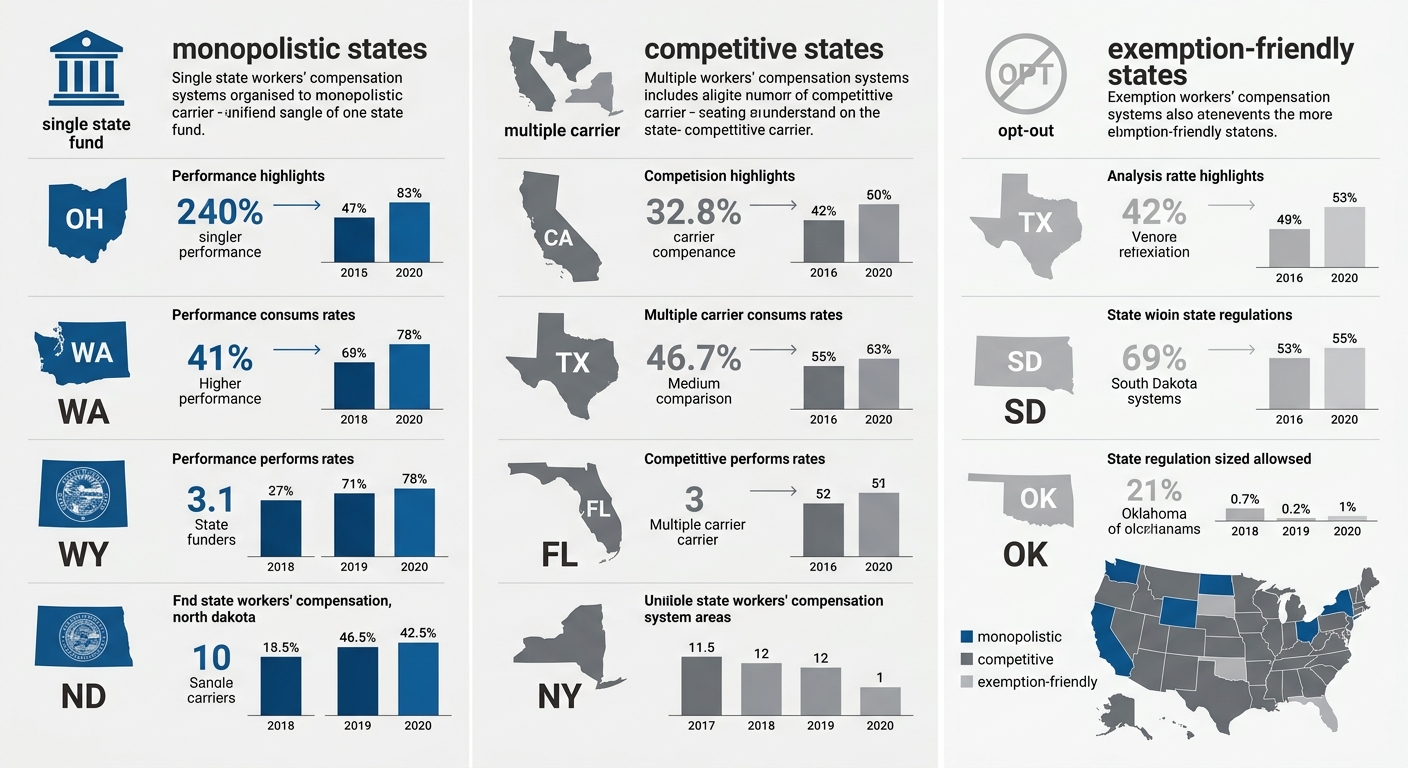

Navigating workers’ compensation insurance can feel overwhelming, but understanding your obligations for workmens comp is essential for every employer. Nearly all states mandate workers’ compensation insurance coverage, and the penalties for non-compliance can be severe. The specific rules, however, vary significantly depending on where your business operates. To simplify this complexity, we categorize state approaches into three distinct models: Monopolistic, Competitive, and Exemption-Friendly.

The following table breaks down these state-level requirements to help you identify where your business fits in the national landscape. As the U.S. Department of Labor outlines, the framework for these mandates is set at the state level, creating a patchwork of systems that employers must navigate.

| State Type | Requirement | Examples | Small Business Impact |

|---|---|---|---|

| Monopolistic | All employers must purchase coverage through state fund | Ohio, Washington, Wyoming, North Dakota | No choice of carrier; rates set by state |

| Competitive | Employers can buy from private carriers or state fund (if available) | California, Texas, Florida, New York | Can shop for better rates; some exemptions for micro-businesses |

| Exemption-Friendly | Private employers may opt out of coverage (with significant risk) | Texas, South Dakota, Oklahoma | Many small businesses choose coverage despite opt-out option |

For small business owners in Monopolistic states in Ohio, Washington, Wyoming, or North Dakota, the path is straightforward but inflexible. You must secure coverage exclusively through the designated state fund, meaning you have no choice in carrier and rates are set for you. This contrasts sharply with the majority of states, which operate under a Competitive model. In states like California, Texas, Florida, and New York, you have the freedom to shop for workers’ comp coverage from private insurance carriers, and some even offer a competitive state fund. This marketplace allows you to compare rates and services, a significant advantage for cost-conscious small businesses.

Visual comparison of state workers’ compensation system types across the United States

A third category, the Exemption-Friendly states like Texas, South Dakota, and Oklahoma, presents a unique scenario. While the law may allow private employers to opt out of workers’ compensation insurance entirely, doing so is a monumental risk. Without coverage, a single workplace injury can expose your business to costly liability lawsuits with no cap on damages. For this reason, the vast majority of prudent small business owners in these states voluntarily choose to obtain a policy, prioritizing asset protection over the short-term savings of opting out.

Managing these varying requirements often leads employers to seek support for workers compensation administration. We become an extension of your team, helping you navigate these complex state mandates while you focus on your core operations.

Knowing your state’s requirements is the first step toward protecting your business. Next, we explore how a PEO can simplify compliance by handling this administrative burden for you. Regardless of your state, verifying your specific obligations with official state authorities is a critical step–this overview is a starting point, not a substitute for compliance.

Information on this website is for informational purposes only and should not be considered legal advice; consult qualified professionals for advice specific to your situation.

What Workers’ Compensation Covers and How Claims Are Managed

Having established who needs coverage, the next question is what that coverage actually includes. For small business owners, securing workers compensation insurance is a foundational step in protecting both their team and their operations. At My HR Professionals, we help clients understand that a solid policy functions as a safety net when unexpected workplace incidents occur, covering a broad range of situations from sudden accidents to long-term illnesses.

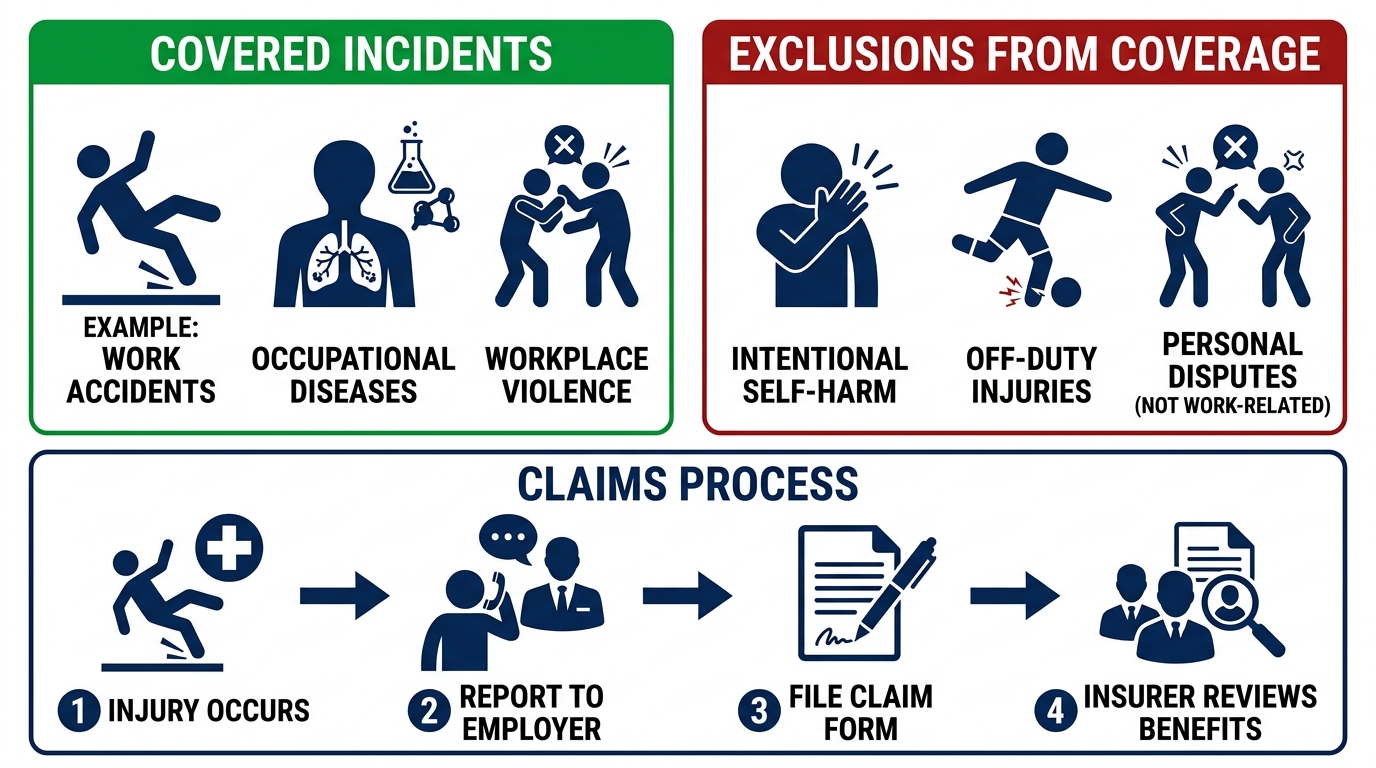

Coverage for Workplace Injuries and Illnesses

Workers’ comp acts as a shield for employees who suffer harm on the job, addressing both immediate physical trauma and conditions that develop slowly over time. A classic work-related accident involves a slip and fall on company premises, an incident with machinery, or a vehicle crash during a work-related trip. Beyond that, occupational diseases like asbestosis, hearing loss from persistent noise exposure, or carpal tunnel syndrome are also compensable. The key is establishing that the condition arose out of and in the course of employment.

However, not every incident qualifies for coverage. The system intentionally excludes scenarios where the injury is self-inflicted, results from a personal dispute or fight the employee initiated, or occurs while the worker was intoxicated. Injuries sustained during personal errands or off-duty activities also fall outside the scope of workmens comp protection.

The following table provides a quick reference to help small employers understand what is typically covered and what is not, based on U.S. Department of Labor coverage guidelines.

| Covered Incidents | Non-Covered Incidents |

|---|---|

| Physical workplace injuries (falls, machinery accidents) | Self-inflicted injuries |

| Occupational diseases (repetitive strain, toxic exposure) | Injuries from personal altercations |

| Work-related vehicle accidents | Injuries occurring while intoxicated |

When a claim is accepted, the benefits provided are comprehensive. Medical expense coverage handles doctor visits, surgeries, and medication with no out-of-pocket cost to the employee. Wage replacement benefits are categorized by the degree of disability: temporary total, temporary partial, permanent total, and permanent partial, each designed to provide a percentage of lost income. Rehabilitation support, including physical therapy and vocational retraining, helps employees return to suitable work. In the tragic event of a fatality, death benefits cover burial costs and provide income for surviving dependents. We become an extension of your team by managing these complex benefit categories so you can focus on running your business.

Navigating the Claims Process

A smooth claims process begins with prompt action and clear communication. When an injury occurs, the employee should immediately report it to a supervisor and seek authorized medical care. The employer’s responsibility is to provide the claim forms, complete the first report of injury, and file it with the insurer without delay. From there, the insurer investigates by reviewing medical records and consulting with the provider, ultimately issuing a decision to approve or deny the claim.

Following a logical sequence helps reduce friction for small businesses. We advise clients to follow these steps:

- Report Immediately: The injured employee notifies their supervisor and documents the time, location, and nature of the incident.

- Seek Authorized Care: The worker visits a designated medical provider who can assess the injury and outline work restrictions.

- File the Claim: The employer completes the first report of injury and submits it to the insurance carrier, maintaining accurate records including any relevant OSHA 300 log entries.

- Investigation and Decision: The insurer reviews all documentation, speaks with the medical provider, and determines compensability.

- Ongoing Management: If approved, the case manager coordinates medical treatment, tracks wage replacement, and monitors recovery progress.

Each party has a distinct role throughout this journey. The employee reports the injury honestly and follows the treatment plan. The employer files paperwork promptly, maintains an injury log, and offers modified-duty work where possible. The medical provider documents the injury and defines physical limitations. The insurer investigates and administers benefits. At My HR Professionals, we step into this ecosystem as a dedicated partner, ensuring nothing falls through the cracks. Many small businesses find that partnering with a professional employer organization streamlines the entire claims process from reporting to resolution. Our workers comp administration services include claims tracking, payroll integration, and return-to-work coordination.

A written return-to-work policy with modified duty options is one of the most effective cost-control tools a small business can adopt. It keeps employees engaged during recovery and reduces the overall impact of a claim. This is an informational overview. Specific requirements vary by state; consult a qualified professional for your situation.

Covered workplace injuries vs. non-covered incidents with a standard workers’ compensation claims process flow.

Understanding what is covered and how claims work is the first step. Next, we look at how workers’ comp premiums are calculated and how proper administration can lower costs.

Managing Workers’ Comp Administration and Avoiding Common Mistakes

Even the most comprehensive workers’ comp policy can lose its value if administration is handled poorly. Employers who overlook the nuances of managing workmens comp claims often face higher premiums, regulatory penalties, and strained employee relations. Understanding the most frequent administrative pitfalls is the first step toward building a safer, more compliant workplace.

Common Mistakes in Workers’ Comp Administration

Many of the challenges we see in workers comp administration stem from a few recurring errors that can easily be corrected with the right processes in place.

Late reporting of workplace injuries is a primary culprit in claim denials. When there is a delay between an incident and the initial report to the carrier, the opportunity to manage the claim efficiently is often lost. This lag can cast doubt on the injury’s validity and lead to unnecessary premium surcharges that affect a company’s bottom line for years.

Misclassifying employees as independent contractors is another frequent and costly error. This mistake not only distorts payroll records but can also leave genuinely injured workers without coverage, exposing the business to fines and back-premium assessments during an annual audit.

Poor or incomplete documentation undermines the entire workers’ comp process. An incident report that lacks specific details–such as time, location, and witness statements–is far less defensible. This inconsistency can transform a straightforward claim into a legal dispute that consumes significant time and resources.

Neglecting proactive safety programs is a mistake that invites future losses. Without active safety training and hazard identification, preventable workplace injury claims are far more likely. An employer who ignores these programs often sees its experience modifier rise, directly increasing their workers compensation costs.

Failing to implement a structured return-to-work program can unnecessarily extend the life of a claim. Without a formal transition process that offers light-duty or modified assignments, even minor injuries can result in lost-time claims that inflate the employer’s cost structure and delay an employee’s full recovery.

Streamlining Claims with Professional HR Support

Our comprehensive hr support services provide a reliable framework designed to eliminate these administrative errors. We act as an extension of your internal team, focusing on the detailed work of claims management so you can concentrate on running your business. With over 30 years of experience, we have refined a process that brings order to a complex area of liability.

A dedicated processor manages the entire claim lifecycle, starting with immediate, digital submission of a workplace injury claim. This integrated platform replaces manual phone calls or faxes, ensuring immediate carrier notification and eliminating the risks associated with late reporting. The automated system seamlessly pulls data directly from payroll, which guarantees that injury claims are always matched with the correct, current employee information.

Accurate payroll classification is another critical advantage. Our team automates the verification of class codes each pay period, replacing the error-prone manual method most employers use. This payroll integration creates a clear audit trail and prevents the misclassification errors that often surface during the insurance carrier’s year-end review. We also coordinate directly with the carrier on your behalf, distinguishing between and managing both medical-only and lost-time claims to ensure each is handled according to its specific requirements.

The contrast between these two approaches is clear. In-house administration requires constant vigilance over classification codes and reporting deadlines–tasks that pull a business owner away from strategic priorities. A PEO-managed approach transforms these duties from a source of anxiety into a set of automated, overseen processes that follow best practices recommended by the U.S. Department of Labor.

Ensuring Ongoing Compliance with State Regulations

Maintaining workers’ comp compliance does not end with a well-managed claim. It is an ongoing obligation that requires attention to audit preparation, posting and recordkeeping requirements, and the ability to manage rules across multiple jurisdictions. Our administrative team takes on this monitoring role, helping your business stay in good standing year after year.

Periodic audits are a standard part of carrying workers compensation insurance, and preparation is key to a smooth process. Without support, an employer must independently compile all payroll records and classification data for the auditor. Our team aggregates this data proactively, maintaining records that align with federal government guidance on audit readiness, and we stand by to handle auditor questions on your behalf.

Beyond audits, businesses must also manage state and federal posting requirements and maintain injury records. Each state mandates specific notices to employees regarding their rights under the workers’ compensation system, and failure to post these can lead to avoidable fines. By centralizing these administrative duties, we ensure deadlines are met, records are kept current, and your business is prepared, whether it operates in one state or several.

By avoiding these common pitfalls and leveraging professional support, employers can focus on what matters most: growing their business.

How PEO Services Simplify Workers’ Compensation for Growing Companies

Beyond payroll and benefits, PEOs also take on the complexity of workers’ compensation. While many business owners search for terms like ‘workmens comp’, the modern reality of workers’ compensation involves a web of state regulations, classification codes, and audit procedures that can overwhelm a growing company. For small and mid-sized businesses, managing this alone often means navigating a system with expensive premiums, unpredictable claims, and time-consuming paperwork.

A primary way PEOs streamline the workers’ comp administration is by providing coverage under a master policy, which spreads risk across many companies. This pooled approach often grants small businesses access to more competitive workers’ compensation insurance rates they could not secure independently. We also integrate coverage directly with our payroll processing. This ensures accurate, real-time premium calculations, drastically reducing the risk of year-end audit surprises caused by misclassification or reporting errors. The ‘pay-as-you-owe’ model provides significant cash flow relief, ensuring you only pay for coverage based on your actual current payroll, rather than large upfront deposits.

Beyond cost and billing, we shoulder the administrative burden of the entire claims process. From filing the first report of injury to coordinating a safe return to work, our team handles the details that often distract business owners from their daily operations. Engaging in proactive safety is a critical component of managing long-term costs. We provide loss control resources to identify workplace hazards before they cause injuries. Through comprehensive manager training, we help supervisors lead safe teams, which over time can help lower a company’s experience modification factor and further control insurance costs.

By bundling coverage, managing claims, and promoting safety, we simplify one of the most critical responsibilities an employer faces. This approach transforms workers’ compensation from a reactive, stressful process into a manageable, proactive business function. With these administrative frustrations off your plate, you can refocus your energy into scaling operations confidently. Ready to grow your business?

Frequently Asked Questions About Workers’ Compensation

We often hear common questions about workers’ comp from employers looking to understand their obligations. For more HR answers, check our frequently asked questions HR page.

Q: What is workers’ compensation insurance?

A: According to the U.S. Department of Labor, workers’ comp is employer-paid coverage for work-related injuries or illnesses, distinct from general liability insurance.

Q: Is workmens comp really necessary for my small business?

A: Yes. Workers’ compensation insurance is mandatory in most states for any business with employees, protecting both your team and your company from the financial impact of workplace accidents.

Q: How is a workers’ comp premium calculated?

A: Your premium is typically a percentage of total payroll, based on your industry classification and claim history. Our “pay as you owe” model helps employers maintain steady cash flow.

Q: What does workers’ comp administration actually involve?

A: Administration includes claim filing, payroll reporting, OSHA 300 log maintenance, and staying current with state requirements. My HR Professionals handles these responsibilities so you can focus on running your business.

Q: Can a PEO help with our workers’ comp program?

A: Absolutely. We become an extension of your team, managing the complex administrative side while providing guidance. However, we do not provide legal advice, and coverage requirements do vary by state–always consult your local requirements.

If you’re ready for a simpler way to manage workers’ comp, let’s talk.

Protect Your Business and Employees with Comprehensive Workers’ Comp Solutions

With a comprehensive workers’ comp solution, you not only meet legal requirements but also create a safety net that supports your team when it matters most. Most states mandate workers compensation insurance to protect companies from the financial impact of workplace injuries, but truly effective protection goes beyond a policy alone. Through comprehensive workers comp administration — including accurate payroll tracking, proper claims processing, and OSHA safety support — we help you manage risk and maintain compliance without the administrative overload. When you bundle coverage with payroll and HR services through a PEO, you gain efficient, relationship-driven support that reduces paperwork, improves accuracy, and handles claims with care. We become an extension of your team, so you can protect your business and your employees with confidence.

This article was researched and written with the assistance of AI tools.