Table of Contents

ERISA Compliance Services Overview

The Employee Retirement Income Security Act (ERISA) of 1974 establishes minimum standards for private-sector employee benefit plans, ensuring fair management and financial soundness, as outlined by authoritative federal guidance from the U.S. Department of Labor. This critical federal layer builds on general employee benefits by imposing strict governance. An ERISA Compliance Service helps employers navigate these complexities, protecting participants and avoiding hefty penalties like up to $1,100 per day for reporting failures.

For sponsors of employee benefits, ERISA mandates fiduciary duties to act solely in participants’ interests and prohibits transactions with parties in interest to prevent conflicts. Plan administrators must fulfill reporting and disclosure obligations, including Summary Plan Descriptions (SPDs), Summary of Material Modifications (SMMs), and participant notifications, per official DOL guidance from the Employee Benefits Security Administration (EBSA). These requirements demand precise adherence to safeguard plan integrity.

Key ERISA compliance services streamline these duties. ERISA wrap documents consolidate multiple plan documents into a single compliant framework, simplifying administration. Form 5500 filing fulfills the core annual reporting need, detailing financials, investments, and operations for plans with 100+ participants, often requiring audits. We handle these with precision to meet deadlines.

Outsourcing ERISA compliance services to experts like My HR Professionals ensures regulatory adherence, minimizes risks, and lets you focus on growth. We become an extension of your team for seamless plan management.

U.S. Department of Labor, eLaws Advisors: ERISA

Employee Benefits Security Administration (EBSA), Reporting and Disclosure Guide for Employee Benefit Plans

ERISA Compliance Fundamentals

Building on ERISA basics, the Employee Retirement Income Security Act of 1974 sets minimum standards for private-sector employee benefit plans, enforced by the U.S. Department of Labor. This law protects participants in retirement and health plans by ensuring fair management and financial soundness. Employers often seek an ERISA Compliance Service to navigate these complexities effectively.

Fiduciaries must uphold duties of prudence, loyalty, and diversification, acting solely in the interest of participants, as outlined in authoritative interactive government guidance from the U.S. Department of Labor. Prohibited transactions prevent conflicts, with penalties up to $1,100 per day for reporting failures like Form 5500 filing.

Annual reporting obligations include Form 5500 filing for pension and welfare plans with 100+ participants, requiring audits and detailing financials, investments, and operations. Retirement plans demand participant disclosures, summary plan descriptions, and bonding, per official DOL standards for administration.

Health plans require robust claims procedures, appeals processes, COBRA continuation coverage, and ERISA wrap documents to ensure compliance with HIPAA and other amendments, as government benchmarks indicate from the U.S. Department of Labor.

Managing these requirements in-house poses challenges like expertise gaps and error risks. The following table compares in-house versus outsourced approaches, data drawn from DOL ERISA resources and My HR Professionals service descriptions:

In-House vs Outsourced ERISA Compliance

Comparison of managing ERISA compliance internally versus through a professional service like those offered by My HR Professionals.

| Aspect | In-House | Outsourced Service |

|---|---|---|

| Requires internal HR experts familiar with ERISA | Access to specialists with 30+ years experience | Dedicated processors and advocates |

| High training and time investment | Scalable, value-focused pricing | Pay as you owe for workers’ comp |

| Potential for penalties from errors | Minimized through proven compliance processes | N/A |

This comparison highlights how outsourcing reduces burdens. In-house management demands significant internal resources, while outsourced options provide specialized knowledge and scalable costs. At My HR Professionals, we leverage our 30+ years of experience from Van Buren, AR, to deliver reliable support, minimizing penalty risks through established processes. Employers gain dedicated advocates who handle filings and documentation seamlessly.

In-house vs outsourced ERISA compliance comparison

Outsourcing to an ERISA Compliance Service like ours ensures fiduciary standards and reporting accuracy. For expert handling of these fundamentals, consider our hr support services to bridge expertise gaps and protect your business.

Deep Dive into ERISA Compliance

Building on ERISA fundamentals, this deep dive into ERISA Compliance Service covers creating compliant ERISA wrap documents for small businesses, their integration with health plans, and key comparisons. We help small employers navigate these requirements to ensure fiduciary duties and reporting obligations are met efficiently.

Creating Compliant ERISA Wrap Plan Documents

Developing compliant ERISA wrap documents starts with understanding your small business health plan’s unique needs. This process ensures a single governing document satisfies ERISA standards, as outlined by authoritative government guidance from the U.S. Department of Labor’s Employee Benefits Security Administration (EBSA).

- Identify plan components: Review insured or self-funded health benefits, including medical, dental, and vision coverage, to list all elements needing ERISA oversight.

- Draft master document with amendments: Create a standardized wrap plan template customized via employer-specific addendums for flexibility without full redesign.

- Integrate Summary Plan Description (SPD): Incorporate clear SPD language detailing participant rights, claims procedures, and eligibility, per EBSA reporting rules.

- Obtain legal review: Engage specialists to verify compliance before distribution, minimizing risks for plans under 100 lives.

A 50-employee firm in Van Buren, AR, streamlines administration this way, saving time on custom drafting.

Next, explore how these documents integrate with employer-sponsored health benefits.

ERISA Wrap Documents for Health Plans

ERISA wrap documents wrap around existing employer-sponsored health benefits, creating a unified ERISA-governed framework. They satisfy fiduciary and reporting duties for insured or self-funded plans, simplifying what small businesses manage daily.

We support this through streamlined employee benefits administration, where wrap plans handle COBRA notices and ACA disclosures alongside core health coverage.

- Wrap around insured plans: Overlay group health policies to establish ERISA jurisdiction, ensuring SPDs and annual reports align with DOL requirements.

- Support self-funded options: Provide fiduciary protections for stop-loss arrangements common in growing firms.

- Handle multi-benefit integration: Combine health, dental, and vision under one document, reducing administrative overlap.

- Facilitate open enrollment: Automate notifications and elections via compliant language.

This approach positions us as an extension of your team for seamless health plan management.

Finally, compare wrap versus individual approaches via this table.

Wrap vs Individual Plan Documents

Small employers weigh ERISA wrap documents against individual plan documents for cost, customization, and risk. Wraps offer efficiencies ideal for businesses like restaurants or trades firms we serve nationwide from Van Buren, AR.

The following table, drawing from DOL health plans guidance and industry best practices, highlights key differences:

| Feature | Wrap Documents | Individual Documents |

|---|---|---|

| Standardized with employer amendments | Fully customized per plan | N/A |

| Lower for small employers | Higher due to complexity | N/A |

| Reduced with service providers | Higher if not expert-drafted | N/A |

Wrap documents lower Form 5500 filing burdens, as official IRS guidelines note simplified annual reporting for wrapped welfare plans. Individual documents demand separate filings per benefit, increasing errors. For compliance risk, wraps leverage provider expertise, per EBSA standards.

We recommend wraps for scalable ERISA compliance, teasing practical implementation in the next section.

Practical ERISA Compliance Strategies

Building on ERISA basics, here are practical Form 5500 filing strategies tailored for small businesses. Outsourcing to an ERISA Compliance Service provider simplifies annual reporting and reduces risks. We recommend bundling these with ERISA wrap documents for comprehensive plan coverage, ensuring fiduciary duties align with U.S. Department of Labor guidelines.

Small businesses benefit from professional handling of Form 5500 requirements, avoiding common pitfalls in participant disclosures and funding standards.

Understanding Form 5500 Filing

Form 5500 serves as the primary annual report for ERISA retirement and welfare benefit plans, as outlined in authoritative government guidelines from the U.S. Department of Labor. Plan administrators must file for plans with 100 or more participants at year-end, or certain small plans under 100 participants that are not fully insured. Fully insured small plans under 100 participants qualify for exemptions per DOL and IRS rules, sparing them from detailed Schedule A filings.

The standard deadline falls on July 31 of the following plan year, with an automatic extension to October 15 available via the Delinquent Filer Voluntary Compliance Program (DF-VCP). This program allows late filings with reduced penalties for eligible plans. According to U.S. Department of Labor standards, administrators bear responsibility for accurate participant counts, financial data, and fiduciary certifications. Small businesses often overlook these nuances, leading to compliance gaps. We at My HR Professionals guide clients through participant thresholds and exemption checks to maintain seamless adherence.

Preparation involves gathering actuarial reports, participant statements, and asset valuations early. Internal Revenue Service procedural data emphasizes complete schedules like SB for single-employer pensions. By understanding these rules upfront, businesses position themselves for efficient e-filing ahead.

E-Filing Form 5500 for ERISA Plans

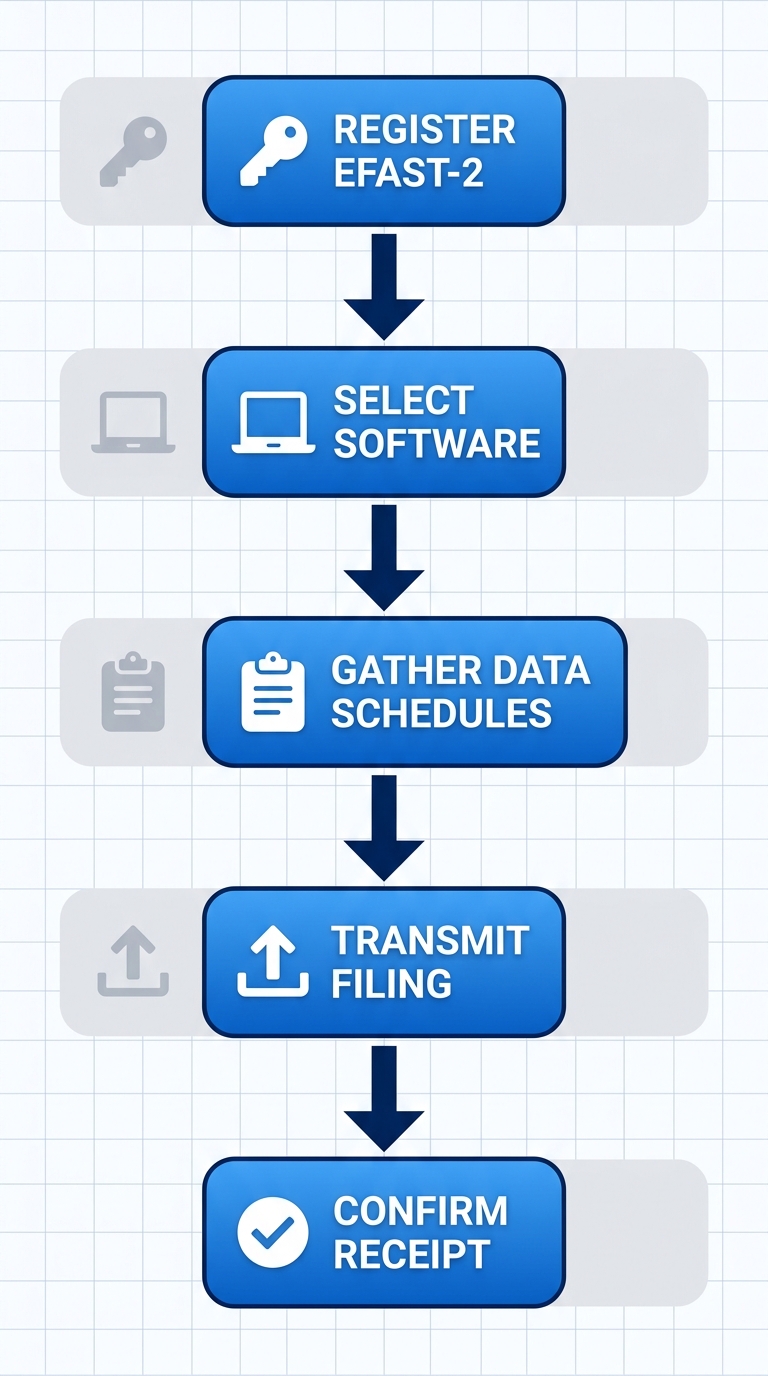

Electronic filing through EFAST-2 is mandatory for most plans, streamlining Form 5500 filing per Internal Revenue Service benchmarks. Follow these steps for success:

- Register for EFAST-2 access via the DOL website, obtaining a sponsor ID and PIN for secure entry.

- Select approved software, such as EFAST-approved tools or third-party vendors for data input.

- Gather required data, including Schedules A, B, and C for insurance, financials, and service provider details.

- Transmit the filing through your provider before the deadline; leverage hr payroll services for seamless transmission and validation.

- Confirm receipt with the EFAST-2 acknowledgment report, retaining it for records.

These steps, drawn from official IRS Form 5500 resources, minimize errors in plan descriptions and funding percentages.

Step-by-step vertical process for ERISA Form 5500 e-filing

This visual reinforces the structured workflow, helping administrators track progress. At My HR Professionals, our dedicated processors handle registrations and data assembly, freeing businesses to focus on operations. Once filed correctly, confirmation ensures audit readiness.

The following table compares Form 5500 filing options, attributed to IRS and DOL guidelines:

| Option | In-House | Professional Service |

|---|---|---|

| Complex software needed | Handled by experts | N/A |

| Risk of missing | Automated reminders | N/A |

| Full liability | Protection via outsourcing | N/A |

In-house efforts demand technical expertise and constant vigilance, while professional services provide expert oversight and safeguards. This contrast highlights why small businesses turn to ERISA compliance solutions for reliability.

Penalties for Late Filings

Late Form 5500 filing triggers severe consequences, with DOL assessing civil penalties up to $2,670 per day per the latest IRS adjustments for inflation. IRS imposes excise taxes of $25 per day, capped at $15,000 per plan, escalating for prolonged delays. U.S. Department of Labor enforcement targets fiduciary lapses, compounding fines with participant lawsuits under ERISA rights.

These penalties strain small business resources, often exceeding thousands annually. Professional ERISA Compliance Service providers mitigate risks through automated tracking, pre-deadline reviews, and DF-VCP submissions. Our error-checking protocols catch discrepancies in schedules, ensuring timely annual 5500 submissions aligned with government benchmarks.

Beyond fines, late filings invite DOL audits and benefit restrictions. Outsourcing shifts liability management to experts, protecting assets. We become an extension of your team, delivering one-stop compliance. These strategies pair well with full-service HR support for ongoing adherence.

Advanced ERISA Compliance Topics

Building on core principles, advanced ERISA compliance topics include complex health plan requirements, wrap documents, and Form 5500 filings. We at My HR Professionals recommend an ERISA Compliance Service to help HR professionals manage these intricacies effectively. According to authoritative U.S. government guidance from the U.S. Department of Labor, ERISA sets minimum standards for private sector health plans, emphasizing fiduciary duties to protect plan assets and participant rights to essential information, grievance processes, and legal recourse for benefit disputes.

ERISA Wrap Documents. These serve as summary plan descriptions (SPDs) for plan amendments, allowing updates without full restatements. Employers use ERISA wrap documents to incorporate changes like HIPAA portability or COBRA continuation coverage. Common pitfalls include incomplete disclosures of fiduciary responsibilities or participant protections, leading to compliance gaps. Proper drafting ensures alignment with DOL standards for transparency and fiduciary accountability.

Form 5500 Filing. Welfare and pension plans with over 100 participants require annual Form 5500 filing through EFAST2 electronic system. The deadline is July 31, with penalties up to $2,670 per day for late submissions. Key steps include:

- Gather participant data and financials.

- Complete schedules for audits if applicable.

- File via EFAST2 with DOL, IRS, and PBGC.

Delays risk enforcement actions, underscoring the need for an ERISA Compliance Service to streamline processes.

Health plan rules demand vigilant oversight of amendments like the Mental Health Parity Act. We integrate technology aids, such as an employee self service portal, for efficient Form 5500 data management. Leveraging an ERISA Compliance Service ensures seamless application of these rules. It also helps document processes, manage audits, and strengthen overall compliance program readiness. Note: This information is for informational purposes only and is not legal advice; consult qualified professionals for your situation.

ERISA Compliance FAQ

Still have questions about our ERISA Compliance Service? See the answers below.

What are ERISA reporting and disclosure requirements?

U.S. Department of Labor’s Employee Benefits Security Administration (EBSA) authoritative federal guidelines require annual filings like Summary Plan Descriptions (SPDs), Summary of Material Modifications (SMMs), and participant notifications for transparency.

What is Form 5500 and who must file it?

Internal Revenue Service (IRS) official resources detail Form 5500 as annual reporting for pension and welfare plans covering 100+ participants. Smaller plans may qualify for exemptions; electronic Form 5500 filing is available.

How does ERISA apply to wrap documents?

ERISA wrap documents integrate with primary plan documents to ensure compliance for benefits like health and welfare. They standardize disclosures and reporting across multiple carriers.

Does ERISA cover workers’ compensation?

Note: ERISA does not cover workmens comp, which falls under state law. We handle exclusions in our ERISA Compliance Service.

Need ERISA Compliance Service? Contact us for expert help.

Achieving ERISA Compliance Success

Building on U.S. Department of Labor guidance for ERISA reporting, disclosure, and fiduciary duties, we at My HR Professionals deliver comprehensive ERISA Compliance Service to simplify compliance for employers nationwide.

We customize ERISA wrap documents to match your plan specifics, ensuring fiduciary compliance and alignment with DOL standards. 1. Tailor documents to welfare benefits. 2. Verify prohibited transaction exemptions. 3. Provide Summary Plan Descriptions. This approach minimizes noncompliance risks like daily penalties up to $1,100.

Our ERISA Compliance Service includes Form 5500 filing support: 1. Compile accurate financial data. 2. Submit electronically via EFAST2. 3. Manage deadlines for audit readiness. U.S. Department of Labor resources confirm these steps protect plans with 100+ participants.

Partner with My HR Professionals for ERISA success. See proven results next.

This article was researched and written with the assistance of AI tools.